Wynn Just Committed $950M to Macau While Its $5.1B UAE Bet Sits in Shipping Limbo

Wynn posted a strong Q1 with $1.86 billion in revenue and beat earnings estimates, then buried the lead: the UAE mega-resort is delayed by geopolitical chaos, and they're doubling down on Macau with a $950M expansion that won't open until 2029.

I've been watching mega-resort development cycles for decades now, and there's a tell that never changes. When a company reports a great quarter and uses the earnings call to announce both a delay on one project and a brand-new commitment somewhere else... that's not confidence. That's portfolio management under pressure. Wynn posted $1.86 billion in Q1 revenue, up 9.2% year-over-year. Net income jumped to $120.5 million from $72.7 million a year ago... a 66% increase. Adjusted EPS of $1.25 beat the street by seven cents. Those are genuinely strong numbers. And yet the stock dropped 4% the next day. Because Wall Street heard exactly what I heard... "modest delay" on a $5.1 billion project in a region where shipping routes are getting rerouted around active conflict zones.

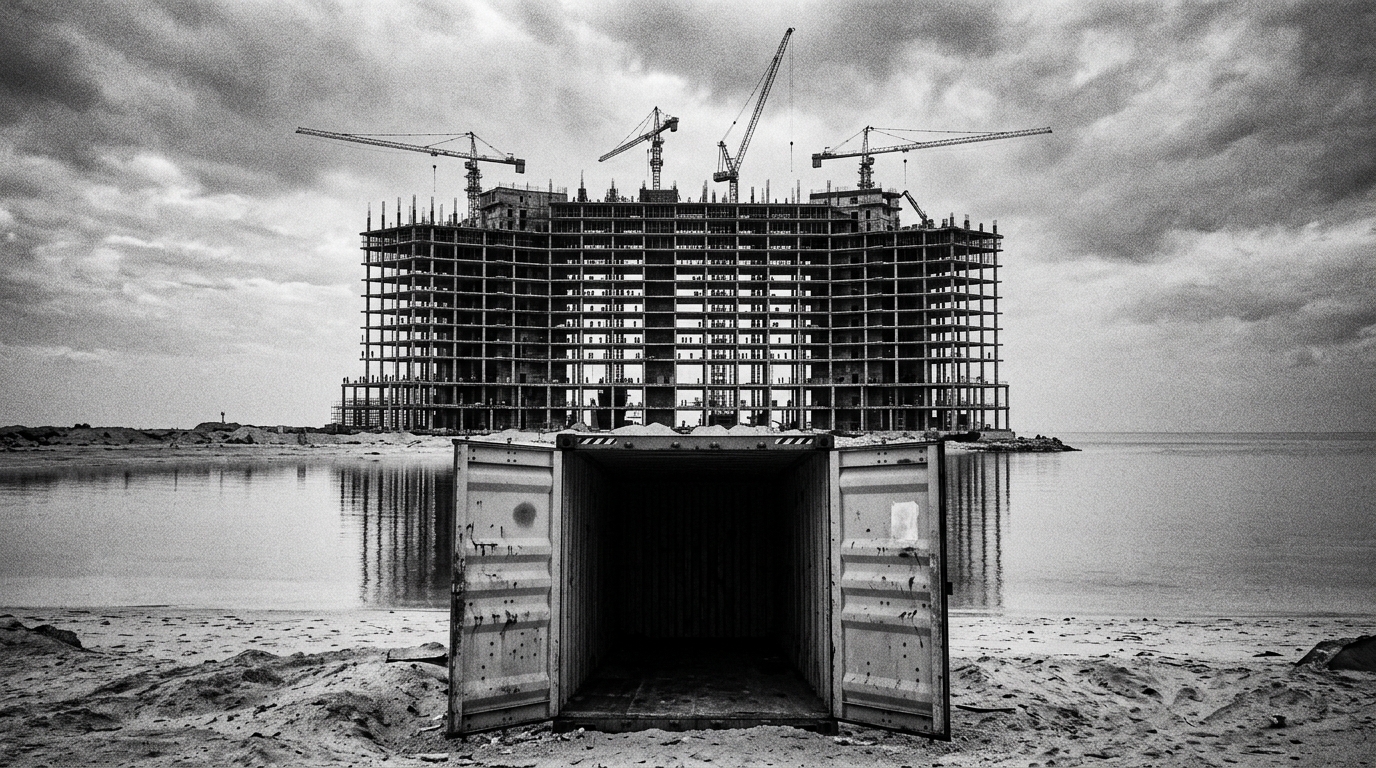

Let me be direct about the UAE situation. Wynn has now poured over a billion dollars in equity into Al Marjan Island with another $350-450 million still to go. They've got 22,000 workers on site. The original early-2027 opening is now... sometime later than that (they're being deliberately vague about the new date, which tells you something). CEO Craig Billings says they underwrote the project with geopolitical risk in mind. I believe him. Smart operators always model downside scenarios. But there's a difference between modeling a risk and living through one where Strait of Hormuz disruptions are forcing construction material reroutes around an active conflict zone. Every rerouted shipment costs more. Every delay compounds. And the carrying cost on a billion-dollar equity commitment isn't theoretical... it's real cash that isn't generating return. Fitch put Ras Al Khaimah on Rating Watch Negative in April. MGM's CEO noted weakened Middle East tourism on their earnings call a week before Wynn's. The signals are all pointing the same direction.

Now here's where it gets interesting. In the same breath, Wynn announces "The Enclave at Wynn Palace" in Macau... 432 all-suite keys, $900-950 million price tag, opening around 2029. That's roughly $2.1 million per key for ultra-luxury suites in a market where Wynn Palace is already running near 100% occupancy. This is the part of the call that deserved more attention than it got. The Macau expansion isn't a hedge against the UAE delay (the timeline doesn't work that way). It's a signal about where Wynn sees its most reliable demand... and it's not the Middle East right now. It's the Chinese luxury traveler who keeps filling their Cotai property. A 25% increase in room count and 50% increase in suite inventory at a property that's already sold out? That math actually makes sense. That's the Wynn I recognize.

What I keep coming back to is the contrast. Two massive capital commitments, two completely different risk profiles. In Macau, you have proven demand, existing infrastructure, established operations, and a regulatory environment Wynn knows intimately. In the UAE, you have a first-of-its-kind gaming license in a region with no track record, construction logistics being disrupted by armed conflict, and the kind of sovereign risk that doesn't show up in a pro forma. I've seen this playbook before... a company with multiple mega-projects at different stages, using the strong performer to give the market patience on the troubled one. The strong Q1 numbers are doing real work here. They're buying Wynn the credibility to say "trust us on the UAE" while everyone watches the carrying costs climb.

The 2029 Macau opening is also worth sitting with for a minute. That's three years of construction spending starting with early piling work this year. Three years is a long time in this industry. A lot can change in Macau's regulatory environment, in Chinese consumer behavior, in the broader luxury travel market. But if you're going to make a billion-dollar bet, making it in a market where you're already sold out every night is about as rational as it gets in the casino resort business. The UAE? That's the swing. It might be brilliant. It might be the most expensive lesson in geopolitical risk management any gaming company has ever received. Right now, nobody knows... including Wynn. And the "modest delay" language tells me they know that you know they don't know.

Look... this story is about a $6 billion gaming company making bets most of us will never make. But the principle underneath it is universal. I've watched operators at every scale commit capital to projects where the assumptions shifted after the check was signed. If you're in any stage of a renovation, expansion, or new build right now, the construction supply chain disruptions Wynn is dealing with in the UAE are a compressed version of what's hitting projects domestically with tariff uncertainty. Call your GC this week. Get an updated materials timeline and cost estimate in writing. Not a verbal "we're on track." In writing. Because if Wynn can't get materials delivered on time to a $5.1 billion project with 22,000 workers, your $3 million lobby renovation isn't immune. What I call the Renovation Reality Multiplier is in full effect right now... the gap between the promised timeline and the actual timeline is wider than it's been in years, and every week of delay has a cost that compounds. Know your real number before someone else tells you what it is.