690 Euros a Night in March. That's What a Single Trade Show Does to Your Comp Set.

Barcelona hotels hit 93% occupancy and a 300% ADR surge during Mobile World Congress, turning a dead winter window into the most profitable week of the year. If your city has a convention center and you're not at the table when they're booking these events, someone else is eating your rate.

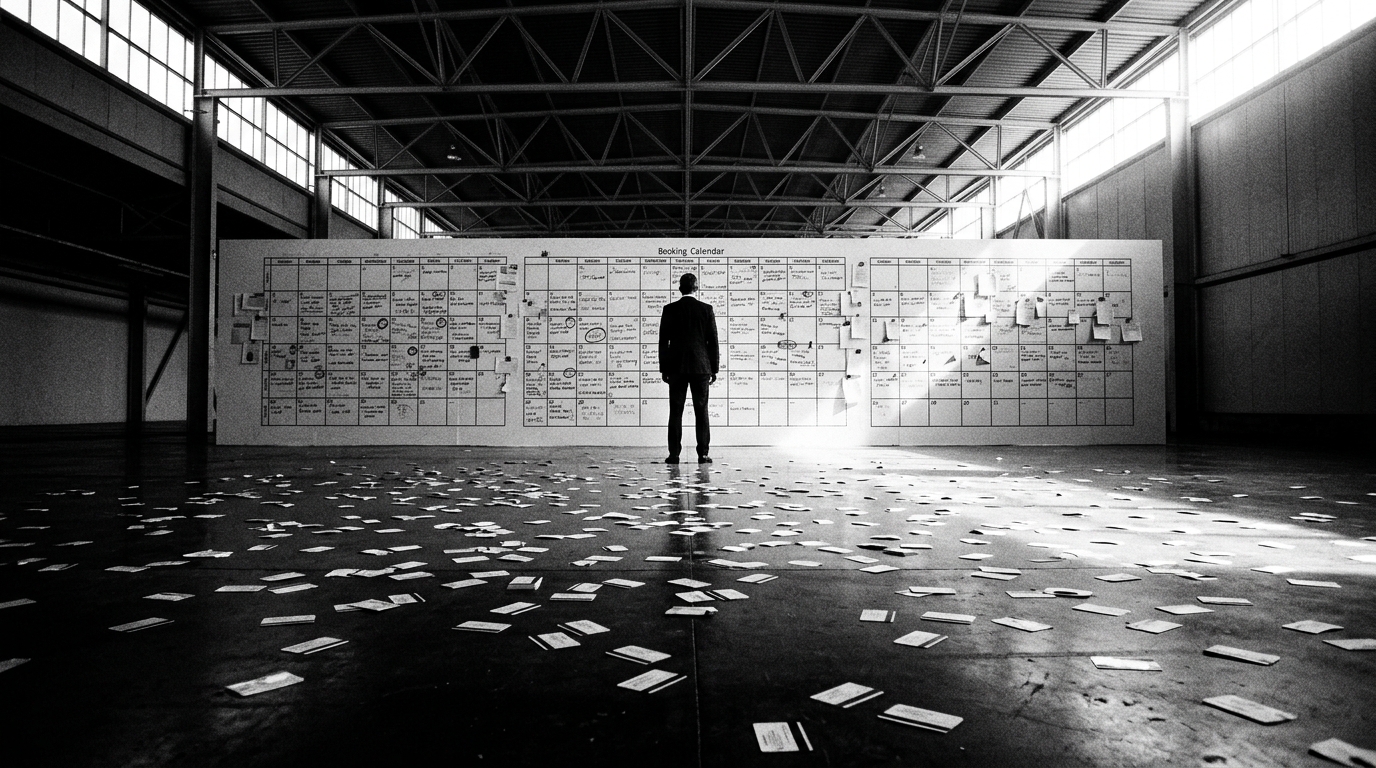

I worked with a GM years ago who kept two calendars on his office wall. One was the hotel's internal forecast. The other was the convention center's booking calendar for the next 18 months. He'd update it himself every quarter by calling his contact at the CVB. His revenue manager thought it was old school. His P&L said otherwise... he was consistently 4-6 points ahead of his comp set on occupancy during convention weeks because he started adjusting strategy 90 days out while everyone else waited for the pickup report to tell them what was already happening.

That's the thing about trade shows. The money is real and it's enormous. Mobile World Congress just pumped 585 million euros into Barcelona in March 2026... a 4.3% bump over 2025. Hotels in the area hit 93% occupancy. Average room rate surged to 690 euros a night. In March. A month when Barcelona hotels normally discount to attract leisure travelers. One event turned a shoulder season into the best revenue week of the quarter. Globally, trade shows drove $180 billion in direct spending last year. This isn't a niche segment. It's a category that reshapes entire markets for a week at a time.

But here's what most operators miss. The headline number is the citywide impact. YOUR number depends entirely on how close you are to the business... literally and strategically. A 500-key full-service three blocks from the convention center with a corporate sales team working the exhibitor list six months out captures a completely different share than a 120-key select-service five miles away hoping for overflow. The ADR premium doesn't distribute evenly across a market. It concentrates. Properties that have relationships with the show organizers, that block rooms for exhibitor groups, that understand the specific needs of trade show travelers (later check-outs, meeting space for side conversations, reliable WiFi that can handle 200 devices per floor)... those properties capture a disproportionate share of the rate surge. Everyone else picks up the scraps and wonders why their RevPAR index didn't move as much as the STR report said the market did.

The other piece nobody talks about is the operational whiplash. Trade show weeks aren't just high-occupancy weeks. They're high-demand, high-expectation, compressed-timeline weeks. You're running at 93% with guests who are on expense accounts, pressed for time, and comparing your property to the last convention hotel they stayed at in Las Vegas or Frankfurt. Your F&B operation needs to be staffed for volume AND speed. Your front desk needs to handle group blocks, walk-ins, and late arrivals simultaneously. Your engineering team needs everything working because the attendee who's paying 690 euros a night has zero tolerance for a broken HVAC unit or spotty internet. If you staff it like a normal high-occupancy night, you'll fill the rooms and tank the reviews. I've seen it happen. Property fills every room, makes great revenue, and spends the next quarter recovering from the guest satisfaction scores because they weren't operationally prepared for the intensity.

The real question for operators isn't whether trade shows are good for hotels. Obviously they are. The question is whether you're positioned to capture the premium or just absorb the chaos. And that answer gets decided months before the event, not the week of.

If you're within five miles of a convention center, your single most valuable relationship outside the building is your CVB contact. Not the tourism marketing person... the convention sales person who knows what's being pitched, what's been signed, and what's coming 12-18 months out. Call them this week. Get on their radar. Ask for the tentative booking calendar and start building your forecast around it. If you're a branded property, don't wait for the brand's demand tools to reflect what you already know is coming... adjust your rate strategy and minimum length-of-stay restrictions 90 days out. And here's the operational piece: build a trade show playbook now. Staffing levels, F&B prep, engineering checklist, WiFi load testing. Have it ready before you need it. The premium only sticks if the guest experience matches the rate. A 300% ADR surge with a two-star review is a one-time windfall. A 300% ADR surge with a guest who rebooks directly next year... that's a revenue engine.