Mark Hoplamazian serves as a key executive at Hyatt Hotels Corporation, one of the major global hospitality operators. His leadership role places him at the center of strategic decisions affecting the company's portfolio, franchise model, and operational direction. Hyatt's asset-light strategy and franchise fee structure represent significant business model considerations for the broader hotel industry.

Hoplamazian has been referenced in recent industry analysis regarding Hyatt's governance practices and corporate structure. These discussions touch on matters relevant to hotel investors and operators evaluating the company's management approach and strategic positioning. His tenure at Hyatt coincides with the company's expansion of its franchise-focused business model, which has implications for capital allocation and revenue generation across the hospitality sector.

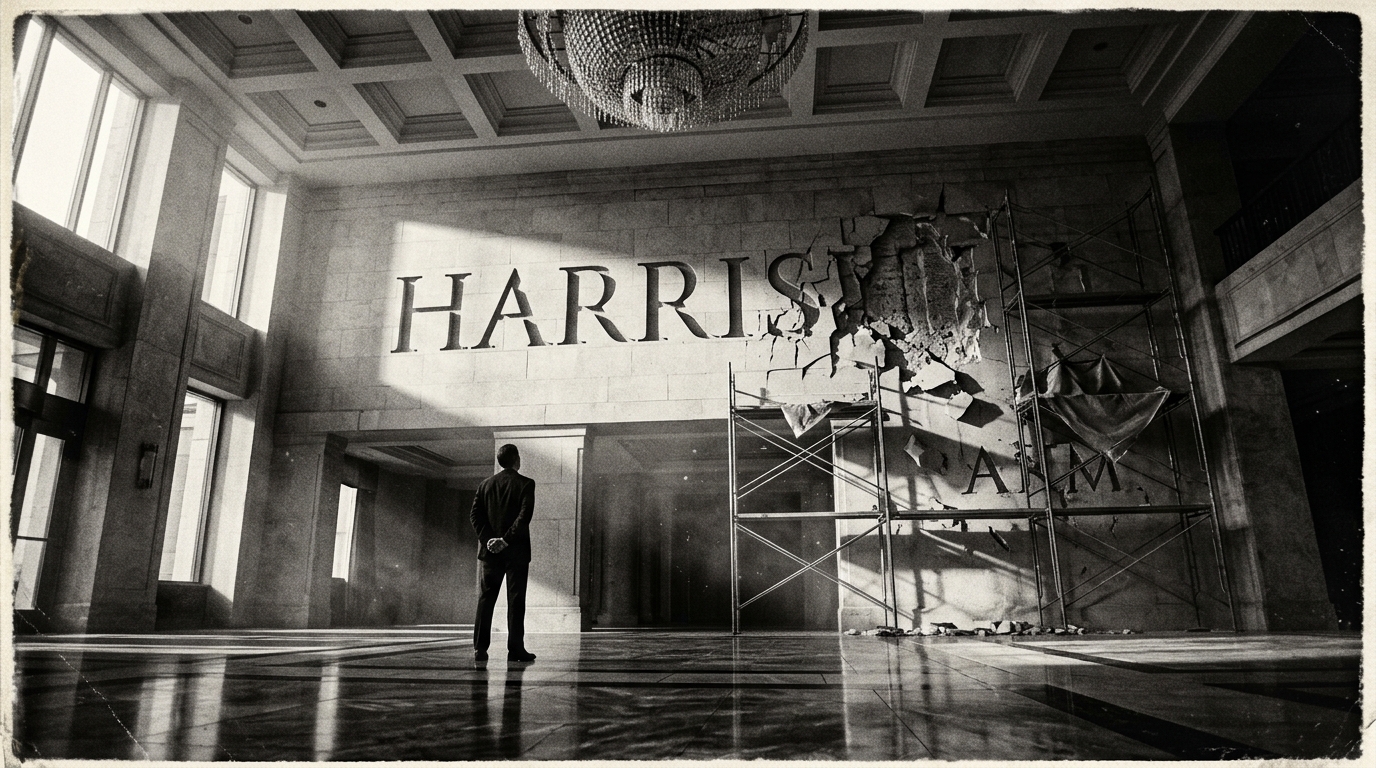

Thomas Pritzker's exit as Hyatt's Executive Chairman wasn't a retirement... it was a reputational emergency triggered by decade-old associations that no technology stack or governance framework could have flagged in time. The real question for every hotel company with a founder's name on the building is what happens when the brand IS a person.

Operations

Primary

Apr 30

Mark Hoplamazian told Bloomberg there are "no signs whatsoever" of consumers pulling back on travel. He's not wrong about his portfolio... but if you're running anything below upper-upscale, his reality and yours are diverging faster than most people realize.

The Pritzker resignation isn't really about Jeffrey Epstein. It's about what happens when the personal life of a family patriarch collides with a publicly traded brand that 1,500 hotels depend on for their identity and their revenue.

📡

Get the Briefing Every Morning at 6AM

Join hotel operators, owners, and investors who start their day with InnBrief.

Free forever. Unsubscribe anytime. No spam — just signal.

Thomas Pritzker's exit as chairman removes the founding family's face from the boardroom, and Wall Street is already gaming out acquisition scenarios. The math on a deal is more interesting than the headlines suggest... and more complicated.

Wall Street loves Hyatt's asset-light pivot and record pipeline. But if you're the one actually running a Hyatt-flagged property, the question isn't whether the stock goes up... it's whether the fees you're paying are earning their keep.

Eighteen brokerages peg Hyatt's average target at $175.80 while the stock sits at $139.38. The 26% gap tells you someone's making a bet on fee-based earnings that hasn't been proven at this scale.

A 4.6% price target reduction on a stock trading at $156 still implies 18.5% upside. The interesting question isn't the target... it's what Morgan Stanley's math assumes about Hyatt's asset-light conversion and whether that assumption survives a downturn.

Three days after their billionaire chairman resigned over connections to convicted sex offenders, Hyatt announced its CFO would present at two major investor conferences. This isn't an investor relations calendar update. This is damage control in a blazer.

The man Hyatt brought in to lead its entire lifestyle strategy just dumped all but 185 shares of his company stock. And nobody at headquarters wants you to notice.

A CEO resigns over ties to a convicted predator. The brand machine mourns leadership. But the real question is why it took this long — and what the franchise agreement says about reputational risk flowing downhill.

Hyatt's Q4 earnings tell a growth story. The franchise agreement tells a different one. Elena Voss reads between the lines.