Anantara's U.S. Debut Has 50 Hotel Suites and 220 Residences. Read That Ratio Again.

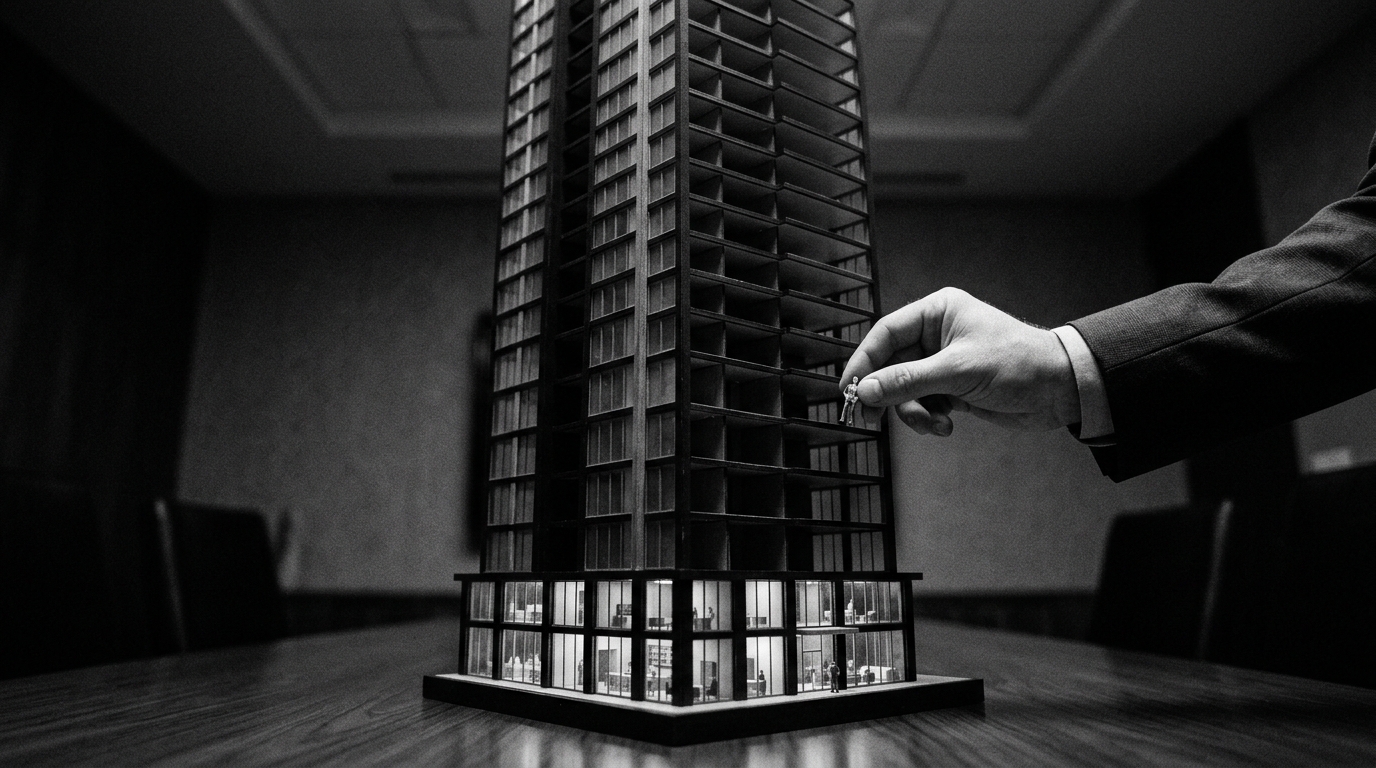

Minor Hotels is launching Anantara in America with a 50-story Miami tower where private residences outnumber hotel rooms more than four to one. The brand promise is "experiential luxury"... but the question is whose experience this building is actually designed to serve.

I grew up in hotels, and my dad was the kind of GM who could look at a building's program and tell you in about ten seconds who it was really built for. Not who the marketing said it was built for. Who was actually going to pay for it, who was going to profit from it, and who was going to be left holding the bag when the renderings stopped matching reality. So when I look at Anantara's Miami debut... 50 hotel suites, 120 "resort residences" that owners can make available to guests, and 100 private branded residences in a 50-story tower opening in 2030... I hear my dad's voice. And he's asking a very specific question: "Is this a hotel, or is this a condo project wearing a hotel's name tag?"

Let's be honest about what's happening here. Minor Hotels, which runs more than 640 properties globally and posted a 32% profit increase last year (THB 6.84 billion, roughly $217 million), has decided that the way to crack the American luxury market is not by building a traditional hotel. It's by building a residential tower with a hospitality wrapper. The math tells you everything. One Sotheby's International Realty is the exclusive sales partner. Residence sales launch later this year. The hotel component... 50 suites... is the smallest slice of the building. And that 120-unit "resort residence" layer? That's a rental pool dressed up in brand language, where individual owners decide whether their units are available to hotel guests on any given night. Which means the GM of this property (God help them) will be managing inventory they don't control, in a building where the majority of occupants aren't hotel guests, with a brand standard designed for resorts in Thailand and the Maldives that now has to translate to an urban tower in Edgewater. I've seen this movie before. Three times, actually. The lobby always looks incredible in the rendering. The operational complexity is always underestimated. And the person who suffers most is the operator trying to deliver a consistent luxury experience when two-thirds of the building answers to individual unit owners, not the hotel.

Here's what the press release doesn't say: branded residences are a brilliant capital strategy and a genuinely difficult hospitality strategy. When 20% of your total pipeline includes a residential component (Minor Hotels' own number), and 50% of your Anantara and Tivoli pipelines include residences, you are not primarily in the hotel business. You are in the real estate branding business. And those are not the same thing, no matter how beautiful the Patricia Urquiola interiors are going to be (and they will be beautiful... her work is extraordinary, this is her first U.S. residential project, and the design press is going to lose its mind). But design is not operations. A rooftop helipad is not a service culture. A "vitality center focused on movement, nutrition, and recovery" is a spa with better copywriting until someone proves otherwise. The Deliverable Test question is simple: can you deliver Anantara-level experiential luxury... the Thai healing traditions, the immersive cultural connection, the holistic wellbeing programming that defines the brand in Koh Samui and the Maldives... in a 50-suite hotel component attached to a 220-unit residential tower in a neighborhood that sits between Wynwood and the Design District? With a staff you haven't hired yet, in a building that won't exist for four years, in a market where every luxury brand on earth is currently fighting for the same high-net-worth guest?

I want to be clear: I'm not saying this won't succeed financially. It very well might. Miami's luxury residential market is absurd right now, the branded residence premium is real (typically 25-35% over comparable unbranded product), and Minor Hotels is smart to use that premium to fund their U.S. market entry. William Heinecke didn't build a 640-property global company by being stupid about capital allocation. But there's a difference between a financially successful real estate project and a brand-defining hotel debut. Minor Hotels is calling this a "defining moment" for their global expansion. They're calling Miami "the perfect location" for Anantara's U.S. entry. And I keep thinking about the gap between what this building will be to the condo buyers (an address, an amenity package, a brand affiliation that looks great on a listing) and what it needs to be for the hotel guest who booked one of 50 suites expecting the Anantara experience they read about in Condé Nast (or saw on "The White Lotus," which is doing more for this brand's American awareness than any marketing budget could). Those are two different promises to two different customers in the same building. And only one of them is going to feel the journey leak when it happens.

The branded residence gold rush is real, and I understand why every luxury brand is chasing it. But I've watched families lose hotels because someone's projections were more compelling than the operating reality that followed. So here's my question for Minor Hotels, and it's the same question my dad would ask: four years from now, when this tower opens and 220 residence owners have opinions about lobby noise and pool access and elevator wait times and whether the hotel guests are "their kind of people"... who's running that building? What does that person's authority actually look like? And does the Anantara brand promise survive a Tuesday night when three residence owners are complaining about the restaurant hours and the hotel guest in suite 4207 expected something they saw on HBO? Because the rendering looks stunning. It always does. The question is what happens at 2 AM.

Here's what I want you thinking about if you're operating in any mixed-use or branded residence environment, or if your brand is pitching you one. The ratio tells you everything. When residences outnumber hotel keys four-to-one, you are not managing a hotel with residences attached... you are managing a residential building with a hotel amenity. Your authority over the guest experience is fundamentally limited by unit owners who have their own ideas about what "their" building should feel like. Before you sign anything, get the HOA governance documents and the management agreement side by side. Map exactly where hotel operations end and residential association authority begins. If there's ambiguity, that ambiguity will cost you. And if your brand is touting a "resort residence rental pool" as inventory you can count on... get the owner opt-in rates in writing, historically, from comparable properties. Because voluntary rental pools in luxury buildings tend to run 40-60% participation at best, and your revenue projections need to reflect that reality, not the optimistic version.